Your credit score is more than just a number—it’s a gateway to financial freedom. Whether you're applying for a loan, renting an apartment, or even job hunting, your credit score affects your opportunities. But if you’re just starting out or trying to rebuild, it can feel like a catch-22: you need credit to build credit. Fortunately, there are proven strategies that can help you build a solid credit history from scratch or improve a low score. This guide outlines the 10 best ways to build credit in the U.S., offering practical steps that are beginner-friendly, effective, and sustainable.

1. Open a Secured Credit Card

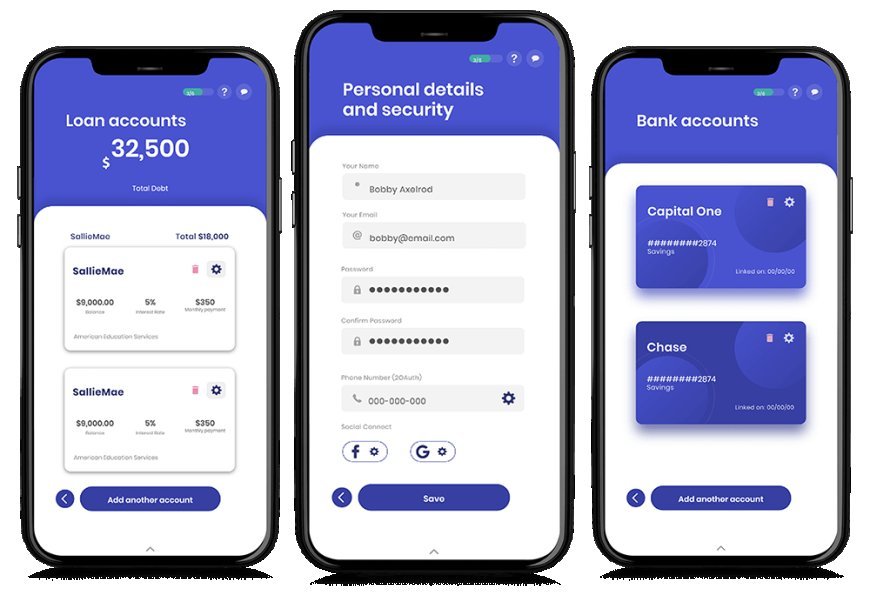

One of the easiest ways to start building credit is with a secured credit card. Unlike regular cards, secured cards require a refundable deposit—usually equal to your credit limit. They report to the major credit bureaus (Equifax, Experian, and TransUnion), helping you establish a credit history when used responsibly.

Continue reading this piece by leonard

Join our community to access the full story. Creating an account is completely free and only takes a moment.

- Read unlimited free publications across the platform

- Directly support independent journalists and authors

- Join discussions, leave reactions, and save your favorites

Responses (0)

Sign in to share your thoughts.

Sign in