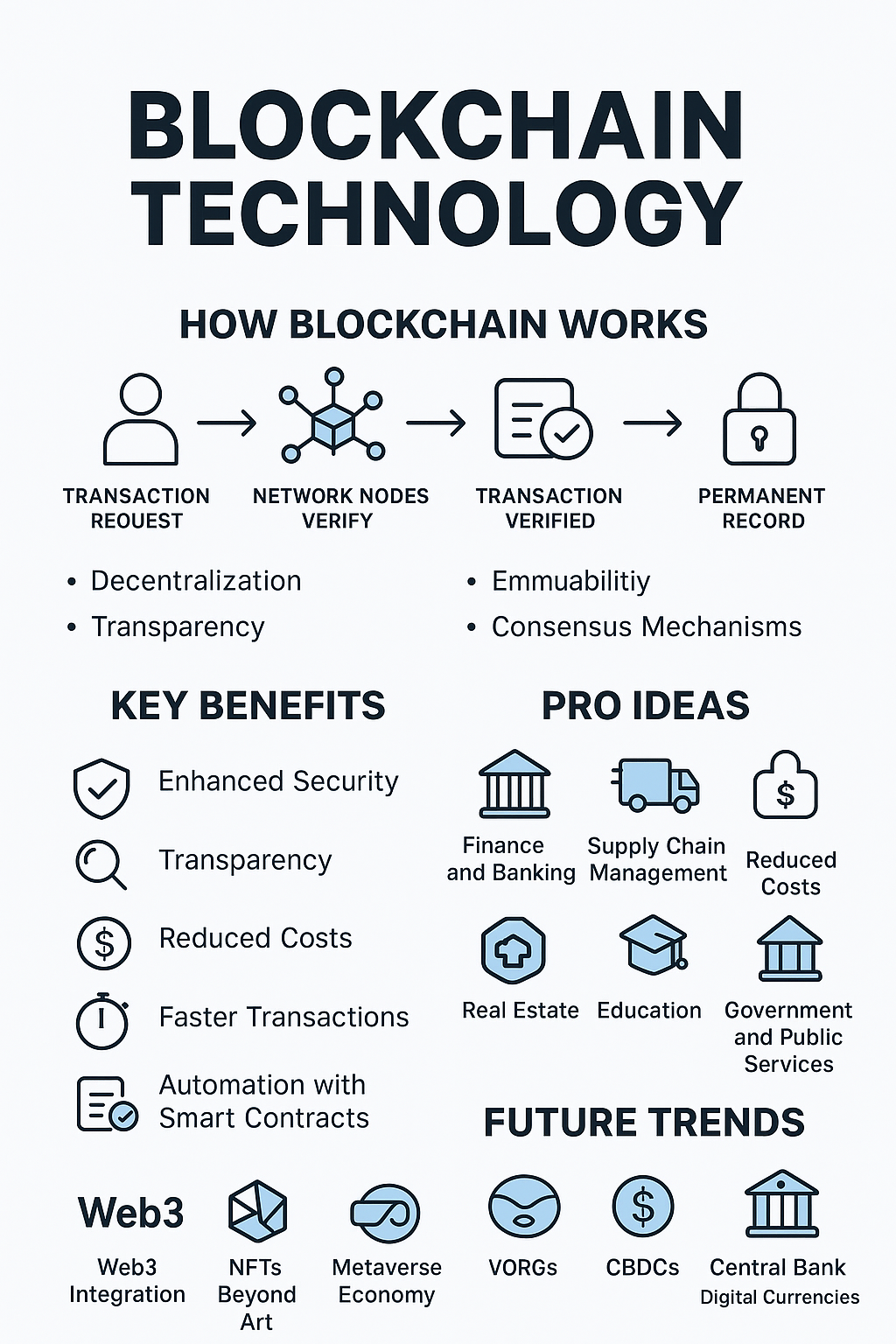

A Comprehensive Guide to Blockchain Technology with Promising Future Ideas,

One of the most ground-breaking innovations of the digital age is blockchain technology. While it initially gained attention as the foundation of cryptocurrencies like Bitcoin, its potential extends far beyond finance. Blockchain promises transparency, security, and efficiency in ways that could reshape industries like healthcare and supply chain management. This article provides an in-depth look at blockchain technology, describing what it is, how it works, its benefits, drawbacks, and professional-level applications.

1. What is Blockchain Technology?

Continue reading this piece by saajan

Join our community to access the full story. Creating an account is completely free and only takes a moment.

- Read unlimited free publications across the platform

- Directly support independent journalists and authors

- Join discussions, leave reactions, and save your favorites

Responses (0)

Sign in to share your thoughts.

Sign in